The Lead In: Enterprise Formation

To maintain this instance as stripped of complexity as I can, at the least to start, I’ll begin with two entrepreneurs who make investments $60 million apiece to start out new companies, albeit with very completely different economics:

- The primary entrepreneur begins enterprise A, with a $60 million funding up entrance, and that enterprise is predicted to generate $15 million in web earnings yearly in perpetuity.

- The second entrepreneur begins enterprise B, once more with a $60 million funding up entrance, and that funding is predicted to generate $3 million yearly in perpetuity.

With these traits, the accounting steadiness sheets for these corporations will likely be an identical proper after they begin up, and the guide worth of fairness will likely be $60 million in every firm.

The return on fairness is a wholly accounting idea, and it may be computed by dividing the web earnings of every of the 2 companies by the guide worth of fairness:

- Return on fairness for Enterprise A = Web earnings for Enterprise A / Ebook Worth of Fairness for Enterprise A = 15/60 = 25%

- Return on fairness for Enterprise B = Web earnings for Enterprise B / Ebook Worth of Fairness for Enterprise B = 3/60 = 5%

Assume that each these companies have the identical underlying enterprise danger that interprets into a value of fairness of 10%, giving the 2 companies the next extra returns:

- Extra Return for Enterprise A = Return on fairness for Enterprise A – Value of fairness for Enterprise A = 25% -10% = 15%

- Extra Return for Enterprise B = Return on fairness for Enterprise B – Value of fairness for Enterprise B = 5% -10% = -5%

Within the language of my final publish, the primary enterprise is an effective one, as a result of it creates worth by incomes greater than your cash would have earned elsewhere on an funding of equal danger, and the second is a foul one, as a result of it doesn’t.

The return on fairness could also be an equation that comes from accounting statements, however in line with my argument that each quantity wants a story, every of those numbers has a story, typically left implicit, that must be made express.

- On enterprise A, the story needs to be considered one of robust boundaries to entry that enable it to maintain its extra returns in perpetuity, and people may embrace something from a superlative model identify to patent safety to unique entry to a pure useful resource. Within the absence of those aggressive benefits, these extra returns would have pale in a short time over time.

- On enterprise B, you might have a problem, because it does appear irrational that an entrepreneur would enter a foul enterprise, and whereas that irrationality can’t be dominated out (maybe the entrepreneur thinks that incomes any revenue makes for a very good enterprise), the fact is that exterior occasions can wreak havoc on the wager paid plans of companies. As an example, it’s attainable that the entrepreneur’s preliminary expectations have been that she or he would earn far more than 5%, however a competitor launching a significantly better product or a regulatory change may have modified these expectations.

In sum, the return on fairness and its extra expansive variant, the return on invested capital, measure what an organization is making on the capital it has invested in enterprise, and is a measure of enterprise high quality.

The Market Launch

Assume now that the homeowners of each companies (A and B) checklist their companies available in the market, disclosing what they anticipate to generate as web earnings in perpetuity. Buyers in fairness markets will now get an opportunity to cost the 2 corporations, and if markets are environment friendly, they’ll arrive on the following:

Thus, a discerning (environment friendly) market would worth enterprise A, with $15 million in web earnings in perpetuity at $150 million, whereas valuing enterprise B, with $3 million in web earnings in perpetuity, at $30 million. In case you are questioning why you’ll low cost web earnings, relatively than money circulate, the distinctive options of those investments (fixed web earnings, no development and endlessly lives) makes web earnings equal to money circulate.

Even with this very simplistic instance, there are helpful implications. The primary is that if markets are environment friendly, the value to guide ratios will replicate the standard of those corporations. On this instance, as an illustration, enterprise A, with a market worth of fairness of $150 million and a guide worth of fairness of $60 million, will commerce at 2.50 occasions guide worth, whereas firm B with a market worth of fairness of $30 million and a guide worth of fairness of $60 million will commerce at half of guide worth. Each corporations can be pretty valued, although the primary trades at effectively above guide worth and the second at effectively beneath, thus explaining why a lazy variant of worth investing, constructed nearly totally on shopping for shares that commerce at low worth to guide ratio,, will lead you to holding unhealthy companies, not undervalued ones.

As I famous at first of this publish, it was motivated by attempting to clear up a basic misunderstanding of what return on fairness measures. The truth is, the working definition that some commenters used for return on fairness was obtained by dividing the web earnings by the market worth of fairness. That’s not return on fairness, however an earnings to cost ratio, i.e., the earnings yield, and in these examples, with no development and perpetual (fixed) web earnings, that earnings yield will likely be equal to the price of fairness in an environment friendly market.

Extending the Dialogue

One of many benefits of this quite simple illustration is that it now can be utilized as a launching pad for casting mild on a few of the most attention-grabbing questions in investing:

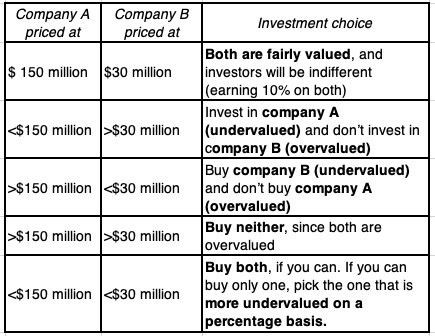

- Good corporations versus Good Investments: I’ve written in regards to the distinction between a very good firm and a very good funding, and this instance gives a straightforward method to illustrate the distinction. corporations A and B, there’s completely no debating the truth that firm A is best firm, with sustainable moats and excessive returns on fairness (25%), than firm B, which struggles to make cash (return on fairness of 5%), and clearly is in a foul enterprise. Nonetheless, which of those two corporations is the higher funding rests totally on how the market costs them:

As you possibly can see, the good firm (A) generally is a good, unhealthy or impartial funding, relying on whether or not its is priced at lower than, better than or equal to its honest worth ($150 million) and the identical might be stated in regards to the unhealthy firm (B), with the value relative to its honest worth ($30 million). At honest worth, each develop into impartial investments, producing returns to shareholders that match their price of fairness.

- The Weakest Hyperlink in Extra Returns: The surplus return is computed because the distinction between return on fairness and the price of fairness, and whereas it’s true that completely different danger and return fashions and variations in danger parameters (relative danger measures and fairness danger premiums) may cause variations in price of fairness calculations, the return on fairness is the weaker hyperlink on this comparability. To grasp a few of the methods the return on fairness might be skewed, contemplate the next variants on the straightforward instance on this case:

- Accounting inconsistencies: As a wholly accounting quantity, the return on fairness is uncovered to accounting inconsistencies and miscategorization. For instance with our easy instance, assume that half the cash invested in enterprise A is in R&D, which accountants expense, as a substitute of capitalizing. That enterprise will report a lack of $15 million (with the R&D expense of $30 million greater than wiping out the revenue of $15 million) within the first yr on guide capital of $30 million (the portion of the capital invested that’s not R&D), however within the years following, it’ll report a return on capital of fifty.00% (since web earnings will revert again to $15 million, and fairness will keep at $30 million). Carrying this by means of to the actual world, you shouldn’t be shocked to see know-how and pharmaceutical corporations, the 2 largest spenders on R&D, report a lot greater accounting returns than they’re really incomes on their investments..

- Growing old belongings: In our instance, we checked out companies an prompt after the upfront funding was made, when the guide worth of funding measures what was paid for the belongings acquired. As belongings age, two tensions seem that may throw off guide worth, the primary being inflation, which if not adjusted for, will consequence within the guide worth being understated, and accounting returns overstated. The opposite is accounting depreciation, which frequently has little to do with financial depreciation (worth misplaced from getting old), and topic to gaming. Extrapolating, initiatives and firms with older belongings will are likely to have overstated accounting returns, as inflation and depreciation lay waste to guide values. The truth is, with an getting old firm, and including in inventory buybacks, the guide worth of fairness can develop into detrimental (and is detrimental for about 10% of the businesses in my firm information pattern).

- Honest Worth Accounting: For the previous few many years, the notion of honest worth accounting has been a fever dream for accounting rule writers, and people guidelines, albeit in patchwork kind, have discovered their manner into company steadiness sheets. In my opinion, honest worth accounting is pointless, and I can use my easy instance for example why. If you happen to marked the belongings of each firm A and firm B to market, you’ll finish with guide values of $150 million and $30 million for the 2 corporations and returns on fairness of 10% for each companies. In brief, if honest worth accounting does what it’s presupposed to do, each agency available in the market will earn a return on fairness (capital) equal to the price of fairness (capital), rendering it ineffective as a metric for separating good and unhealthy companies. If honest worth accounting fails at what it’s presupposed to do, which is the extra possible state of affairs, you’ll find yourself with guide values of fairness that measure neither authentic capital invested nor present market worth, and returns on fairness and capital that develop into noise.

Conclusion

Lots of the feedback on my seventh information replace, and on my clarification about why ROE and value of fairness don’t must be equal in an environment friendly market, got here from individuals with levels and certifications in finance, and fairly a couple of of the commenters had “finance skilled” listed of their profile. Quite than take subject with them, I might argue that this misunderstanding of fundamentals is a damning indictment of how these ideas and subjects are taught within the classroom, and since I could very effectively be one of many culprits, one motive that I wrote this publish is to remind myself that I’ve to revisit the fundamentals, earlier than making formidable leaps into company monetary evaluation and valuation. For these of you who should not finance professionals, however depend on them for recommendation, I hope it is a cautionary word on taking these professionals (consultants, appraisers, bankers) at their phrase. A few of them throw buzzwords and metrics round, with little understanding of what they imply and the way they’re associated, and it’s caveat emptor.

YouTube Video