Just a few weeks in the past, I posted on the company life cycle, the topic of my newest guide. I argued that the company life cycle can clarify what occurs to firms as they age, and why they need to adapt to growing older with their actions and selections. In parallel, I additionally famous that buyers have to vary the best way they worth and value firms, to mirror the place they’re within the life cycle, and the way totally different funding philosophies lead you to concentrated picks in several phases of the life cycle. Within the closing part, I contended that managing and investing in firms turns into most tough when firms enter the final phases of their life cycles, with revenues stagnating and even declining and margins underneath strain. Whereas consultants, bankers and even some buyers push firms to reinvent themselves, and discover development once more, the reality is that for many firms, the very best pathway, when dealing with growing older, is to simply accept decline, shrink and even shut down. On this submit, I’ll take a look at three excessive profile firms, Intel, Starbucks and Walgreens, which have seen market turmoil and administration change, and look at what the choices are for the long run.

Setting the stage

The three firms that I picked for this submit on decline current very totally different portraits. Intel was a tech celebrity not that way back, an organization based by Gordon Moore, Robert Noyce and Arthur Rock in 1968, whose laptop chips have helped create the tech revolution. Walgreens is an American establishment, based in Chicago in 1901, and after its merger with Alliance Boots in 2014, one of many largest pharmacy chains within the nation. Lastly, Starbucks, which was born in 1971 as a espresso bean wholesaler in Pike Place Market in Seattle, was transformed right into a espresso store chain by Howard Schultz, and to the dismay of Italians, has redefined espresso drinks all over the world. Whereas they’re in very totally different companies, what they share in widespread is that over the latest yr or two, they’ve all not solely misplaced favor in monetary markets, however have additionally seen their enterprise fashions come underneath menace, with their working metrics (income development, margins) reflecting that menace.

The Market turns

With a whole bunch of shares listed and traded available in the market, why am I listening to these three? First, the businesses are acquainted names. Our private computes are sometimes Intel-chip powered, there’s a Walgreen’s a couple of blocks from my house, and all of us have a Starbucks across the nook from the place we dwell and work. Second, they’ve all been within the information in the previous couple of weeks, with Starbucks getting a brand new CEO, Walgreens saying that they are going to be shutting down a whole bunch of their shops and Intel developing within the Nvidia dialog, typically as a distinction. Third, they’ve all seen the market flip in opposition to them, although Starbucks has had a comeback after its new CEO rent.

Not one of the three shares has been a winner during the last 5 years, however the decline in Intel and Walgreen’s has been precipitous, particularly int he final three years. That decline has drawn the standard suspects. On the one hand are the knee-jerk contrarians, to whom a drop of this magnitude is at all times a chance to purchase, and on the opposite are the apocalyptists, the place massive value declines virtually at all times finish in demise. I’m not a fan of both excessive, however it’s simple that each teams can be proper on some shares, and incorrect on others, and the one option to inform the distinction is to take a look at every of the businesses in additional depth.

A Tech Star Stumbles: Intel’s Endgame

In my guide on company life cycles, I famous that even celebrity firms age and lose their luster, and Intel might be a case research. The corporate is fifty six years outdated (it was based in 1968) and the query is whether or not its finest years are behind it. Actually, the corporate’s development within the Nineties to succeed in the height of the semiconductor enterprise is the stuff of case research, and it stayed on the high for longer than most of its tech contemporaries. Intel’s CEO for its glory years was Andy Grove, who joined the corporate on its date of incorporation in 1968, and stayed on to change into chairman and CEO earlier than stepping down in 1998. He argued for fixed experimentation and adaptive management, and the title of his guide, “Solely the Paranoid Survive”, captured his administration ethos.

To get a measure of why Intel’s fortunes have modified within the final decade, it’s price taking a look at its key working metrics – revenues, gross earnings and working earnings – over time:

As you may see on this graph, Intel’s present troubles didn’t happen in a single day, and its change over time is sort of textbook company life cycle. As Intel has scaled up as an organization, its income development has slackened and its development charge within the final decade (2012-21) is extra reflective of a mature firm than a development firm. That stated, it was a wholesome and worthwhile firm throughout that decade, with stable unit economics (as mirrored in its excessive gross margin) and profitability (its working margin was greater within the final decade than in prior intervals). Within the final three years, although, the underside appears to fallen out of Intel’s enterprise mannequin, as revenues have shrunk and margins have collapsed. The market has responded accordingly, and Intel, which stood on the high of the semiconductor enterprise, when it comes to market capitalization for nearly three a long time, has dropped off the record of high ten semiconductor firms in 2024, in market cap phrases:

Intel’s troubles can’t be blamed on industry-wide points, since Intel’s decline has occurred on the similar time (2022-2024) because the cumulative market capitalization of semiconductor firms has risen, and certainly one of its peer group (Nvidia) has carried the market to new heights.

Earlier than you blame the administration of Intel for not attempting arduous sufficient to cease its decline, it’s price noting that if something, they’ve been attempting too arduous. In the previous couple of years, Intel has invested large quantities into its chip manufacturing enterprise (Intel Foundry), attempting to compete with TSMC, and virtually as a lot into its new era of AI chips, hoping to say market share of the quickest rising markets for AI chips from Nvidia. Actually, a benign evaluation of Intel could be that they’re making the correct strikes, however that these strikes will take time to repay, and that the market is being impatient. A not-so-benign studying is that the market doesn’t consider that Intel can compete successfully in opposition to both TSMC (on chip manufacture) or Nvidia (on AI chip design), and that the cash spent on each endeavors can be wasted. The latter group is clearly profitable out in markets, in the mean time, however as I’ll argue within the subsequent part, the query of whether or not Intel is an effective funding at its present depressed value might relaxation through which group you assume has proper on its facet.

Drugstore Blues: Walgreen Wobbles

From humble beginnings in Chicago, Walgreen has grown to change into a key a part of the US well being care system as a dispenser of pharmacy medicine and merchandise. The corporate went public in 1927, and within the century since, the corporate has acquired the traits of a mature firm, with development spurts alongside the best way. Its acquisition of a big stake in Alliance Boots gave it a bigger international presence, albeit at a excessive value, with the acquisition costing $15.3 billion. Once more, to know, Walgreen’s present place, we seemed on the firm’s working historical past by trying income development and revenue margins over time:

After double digit development from 1994 to 2011, the corporate has struggled to develop in a enterprise, with daunting unit economics and slim working margins, and the final three years have solely seen issues worsen on all fronts, with income development down, and margins slipping additional, under the Maginot line; with an 1.88% working margin, it’s inconceivable to generate sufficient to cowl curiosity bills and taxes, thus triggering misery.

Whereas administration selections have clearly contributed to the issues, additionally it is true that the pharmacy enterprise, which types Walgreen’s core, has deteriorated during the last two years, and that may be seen by evaluating its market efficiency to CVS, its highest profile competitor.

Venti no extra The Humbling of Starbucks

On my final go to to Italy, I did make frequent stops at native cafes, to get my espresso pictures, and I can say with confidence that none of them had a caramel macchiato or an iced brown sugar oatmilk shaken espresso on the menu. A lot as we make enjoyable of the myriad choices at Starbucks, it’s simple that the corporate has discovered a approach into the each day lives of many individuals, whose day can’t start with out their favourite Starbucks drink in hand. Early on, Starbucks eased the method by opening increasingly more shops, typically inside blocks of one another, and extra lately, by providing on-line ordering and decide up, with rewards supercharging the method. Howard Schultz, who nursed the corporate from a single retailer entrance in Seattle to an ubiquitous presence throughout America, was CEO of the corporate from 1986, and whereas he retired from the place in 2000, he returned from 2008 to 2017, to revive the corporate after the monetary disaster, and once more from 2022 to 2023, as an interim CEO to bridge the hole between the retirement of Kevin Johnson in 2022 and the hiring of Laxman Narasimhan in 2023. To get a measure of how Starbucks has developed over time, I seemed the revenues and margins on the firm, over time:

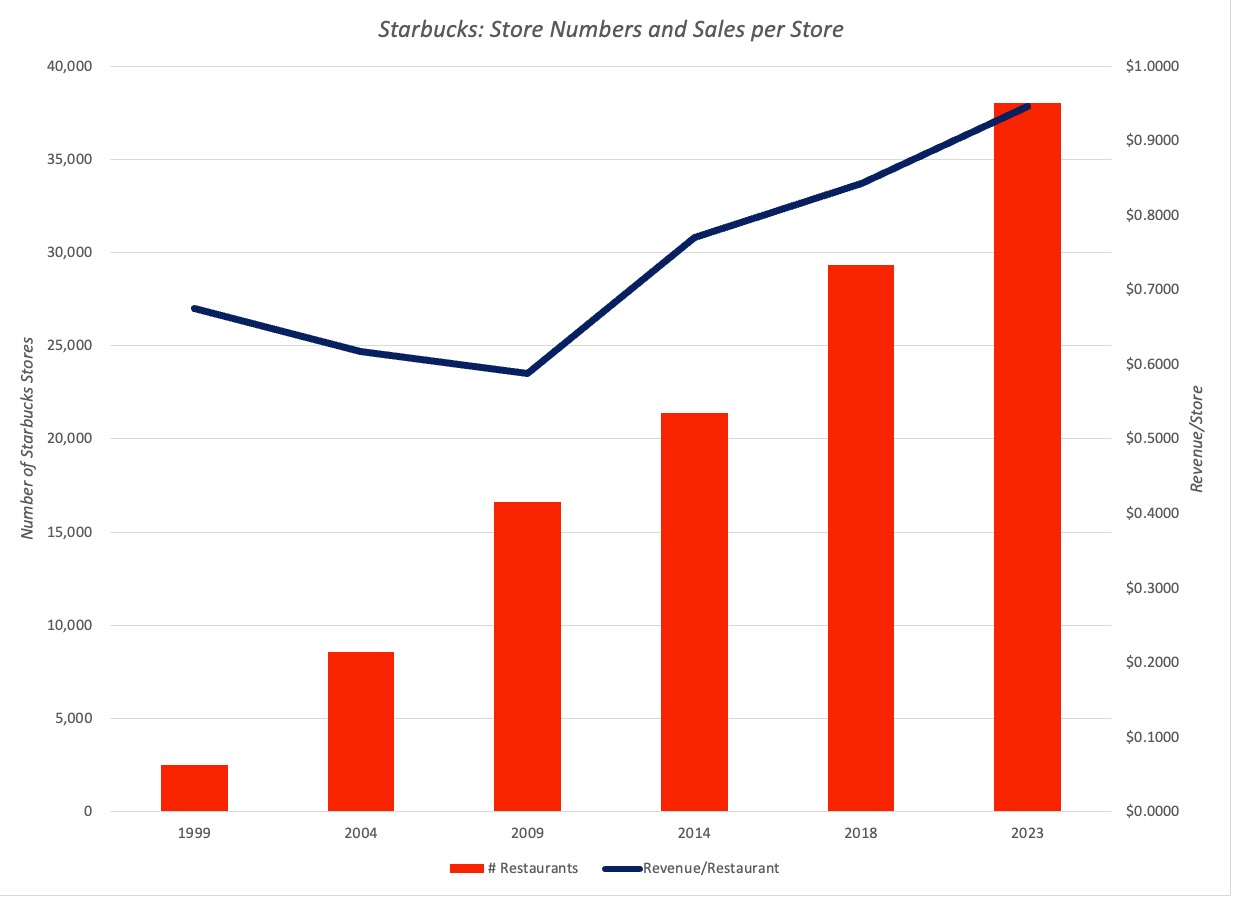

Not like Intel and Walgreens, the place the growing older sample (of slowing development and steadying margins) is clearly seen, Starbucks is a more durable case. Income development at Starbucks has slackened over time, but it surely has remained strong even in the newest interval (2022-2024). Revenue margins have truly improved over time, and are a lot greater than they have been within the first twenty years of the corporate’s existence. One motive for bettering profitability is that the corporate has change into extra cautious about retailer openings, at the very least in america, and gross sales have elevated on a per-store foundation:

Actually, the shift in the direction of on-line ordering has accelerated this development, since there’s much less want for expansive retailer places, if a 3rd or extra of gross sales come from clients ordering on-line, and selecting up their orders. In brief, these graphs counsel that it’s unfair to lump Starbuck with Intel and Walgreens, since its struggles are extra reflecting of a development firm dealing with center age.

So, why the market angst? The primary is that there are some Starbucks buyers who proceed to carry on to the hope that the corporate will be capable to return to double digit development, and the one pathway to get there requires that Starbucks be capable to reach China and India. Nevertheless, Starbucks has had hassle in China competing with home lower-priced opponents (Luckin’ Espresso and others), and there are restrictions on what Starbucks can do with its three way partnership with the Tata Group in India. The second drawback is that the narrative for the corporate, that Howard Schultz bought the market on, the place espresso outlets change into a gathering spot for mates and acquaintances, has damaged down, partly due to the success of its on-line ordering enlargement. The third drawback is that inflation in product and worker prices has made its merchandise costly, resulting in much less spending even from its most loyal clients.

A Life Cycle Perspective

It’s simple that Intel and Walgreens are in hassle, not simply with markets however operationally, and Starbucks is scuffling with its story line. Nevertheless, they face totally different challenges, and maybe totally different pathways going ahead. To make that evaluation, I’ll extra use my company life cycle framework, with a particular emphasis on the the alternatives that agin firms face, with determinants on what ought to drive these selections.

The Company Life Cycle

I will not bore you with the small print, however the company life cycle resembles the human life cycle, with start-ups (as infants), very younger firms (as toddlers), excessive development firms (as youngsters) transferring on to mature firms (in center age) and outdated firms dealing with decline and demise:

The section of the life cycle that this submit is targeted on is the final one, and as we are going to see within the subsequent part, it’s the most tough one to navigate, partly as a result of shrinking as a agency is considered as failure., and that lesson will get strengthened in enterprise faculties and books about enterprise success. I’ve argued that extra money is wasted by firms refusing to behave their age, and far of that waste happens within the decline section, as firms desperately attempt to discover their approach again to their youth, and bankers and consultants egg them on.

The Selections

There isn’t a tougher section of an organization’s life to navigate than decline, since you might be typically confronted with unappetizing selections. Given how badly we (as human beings) face growing older, it ought to come as no shock that firms (that are entities nonetheless run by human beings) additionally combat growing older, typically in damaging methods. On this part, I’ll begin with what I consider are probably the most damaging selections made by declining companies, transfer on to a middling selection (the place there’s a chance of success) earlier than inspecting probably the most constructive responses to growing older.

a. Harmful

- Denial: When administration of a declining enterprise is in denial about its issues, attributing the decline in revenues and revenue margins to extraordinary circumstances, macro developments or unhealthy luck, it can act accordingly, staying with current practices on investing, financing and dividends. If that administration stays in place, the reality will finally meet up with the corporate, however not earlier than extra money has been sunk into a nasty enterprise that’s un-investable.

- Desperation: Administration could also be conscious that their enterprise is in decline, however it could be incentivized, by cash or fame, to make large bets (acquisitions, for instance), with low odds, hoping for successful. Whereas the house owners of those companies lose a lot of the time, the managers who get hits change into superstars (and get labeled as turnaround specialists) and enhance their incomes energy, maybe at different companies.

- Survival at any value: In some declining companies, high managers consider that it’s company survival that ought to be given precedence over company well being, they usually act accordingly. Within the course of, they create zombie or strolling lifeless firms that survive, however as unhealthy companies that shed worth over time.

b. It relies upon

- Me-too-ism: On this selection, administration begins with consciousness that their current enterprise mannequin has run out of gasoline and faces decline, however consider {that a} pathway exists again to well being (and even perhaps development) if they will imitate the extra profitable gamers of their peer teams. Consequently, their investments can be directed in the direction of the markets or merchandise the place success has been discovered (albeit by others), and financing and money return insurance policies will comply with. Many companies undertake this technique discover themselves at an obstacle, since they’re late to the celebration, and the winners typically have moats which are tough to broach or a head begin that can’t be overcome. For a couple of companies, imitation does present a respite and at the very least a brief return to mature development, if not excessive development.

c. Constructive

- Acceptance: Some companies settle for that their enterprise is in decline and that reversing that decline is both inconceivable to do or will value an excessive amount of capital. They comply with up by divesting poor-performing belongings, spinning off or splitting off their better-performing companies, paying down debt and returning more money to the house owners. If they will, they settle in on being smaller companies that may proceed to function in subparts of their outdated enterprise, the place they will nonetheless create worth, and if this isn’t attainable, they’ll liquidate and exit of enterprise.

- Renewals and Revamps: In a renewal (the place an organization spruces up its current merchandise to enchantment to a bigger market) or a revamp (the place it provides to its merchandise and repair providing to make them extra interesting), the hope is that the market is massive sufficient to permit for a return to regular development and profitability. To drag this off, managers need to be clear eyed about what they provide clients, and acknowledge that they can’t abandon or neglect their current buyer base of their zeal to search out new ones.

- Rebirths: That is maybe each declining firm’s dream, the place you’ll find a brand new market or product that may reset the place the corporate within the life cycle. This pitch is powered by case research of firms which have succeeded in pulling off this feat (Apple with the iPhone, Microsoft with Azure), however these successes are uncommon and tough to duplicate. Whereas one can level to widespread options together with visionary administration and natural development (the place the brand new enterprise is constructed inside the firm somewhat than acquired), there’s a robust component of luck even within the success tales.

The Determinants

Clearly, not all declining firms undertake the identical pathway, when confronted with decline, and extra firms, for my part, take the damaging paths than the constructive one. To know why and the way declining firms select to do what they do, it’s possible you’ll wish to contemplate the next:

- The Enterprise: A declining firm in an in any other case wholesome {industry} or market has higher odds for survival and restoration than one that’s in a declining {industry} or unhealthy enterprise. With the three firms in our dialogue, Intel’s troubles make it an outlier in an in any other case wholesome and worthwhile enterprise (semiconductors), whereas Walgreens operates in a enterprise (brick and mortar retail and pharmacy) that’s wounded. Lastly, the challenges that Starbucks faces of a saturated market and altering buyer calls for is widespread to massive eating places in america.

- Firm’s strengths: An organization that’s in decline might have fewer moats than it used to, however it could nonetheless maintain on to its remaining strengths that draw on them to combat decline. Thus, Intel, regardless of its troubles in recent times, has technological strengths (individuals, patents) which may be underneath utilized proper now, and if redirected, might add worth. Starbucks stays among the many most acknowledged restaurant manufacturers on this planet, however Walgreens regardless of its ubiquity in america, has virtually no differentiating benefits.

- Governance: The choices on what a declining agency ought to do, within the face of decline, are usually not made by its house owners, however by its managers. If managers have sufficient pores and skin within the sport, i.e., fairness stakes within the firm, their selections can be typically very totally different than if they don’t. Actually, in lots of firms with dispersed shareholding, administration incentives (on compensation and recognition) encourage resolution makers to go for long-shot bets, since they profit considerably (personally) if these bets repay and the draw back is funded by different individuals’s cash.

- Buyers: With publicly traded firms, it’s the buyers who in the end change into the wild card, figuring out time horizon and possible choices for the corporate. To the extent that the buyers in a declining firm need fast payoffs, there can be strain for firms to simply accept growing older, and shrink or liquidate; that’s what personal fairness buyers with sufficient clout carry to the desk. In distinction, if the buyers in a declining firm have for much longer time horizons and see advantages from a turnaround, you usually tend to see revamps and renewals. All three of the businesses in our combine are institutionally held, and even at Starbucks, Howard Schultz owns lower than 2% of the shares. and his affect comes extra from his standing as founder and visionary than from his shareholding.

- Exterior elements: Corporations don’t function in vacuums, and capital markets and governments can change into determinants of what they do, when confronted with decline. Usually, firms that function in liquid capital markets, the place there are a number of paths to boost capital, have extra choices than firms than function in markets the place capital is scare or tough to boost. Governments can also play a task, as we noticed within the aftermath of the 2008 disaster, when assist (and funding) flowed to firms that have been too massive to fail, and that we see frequently in companies just like the airways, the place even probably the most broken airline firms are allowed to limp alongside.

- Luck: A lot as we wish to consider that our fates are in our personal palms, the reality is that even the best-thought by response to say no wants a hearty dose of luck to succeed.

Within the determine under, I summarize the dialogue from this part, taking a look at each the alternatives that firms could make, and the determinants:

With this framework in place, I’m going to attempt to make my finest judgments (which you’ll disagree with) on what the three firms highlighted on this submit ought to do, and the way they’ll play out for me, as an investor:

- Intel: It’s my view that Intel’s issues stem largely from an excessive amount of me-too-ism and aspiring for development ranges that they can’t attain. On each Ai and the chip manufacturing enterprise, Intel goes up in opposition to competitors (Nvidia on AI and TSMC on manufacturing) that has a transparent lead and important aggressive benefits. Nevertheless, the market is massive sufficient and has enough development for Intel to discover a place in each, however not as a pacesetter. For a corporation that’s used to being on the high of the leaderboard, that can be a step down, however much less ambition and extra focus is what matches the corporate, at this stage within the life cycle. It’s doubtless that even when it succeeds, Intel will revert to center age, not excessive development, however that ought to nonetheless make it an excellent funding. Within the desk under, you may see that at its prevailing inventory value of $18.89 (on Sept 8, 2024), all you want is a reversion again in the direction of extra regular margins for the worth to be justified:With 3% development and 25% working margins, Intel’s worth per share is already at $23.70 and any success that the corporate is within the AI chip market or advantages it derives from the CHIPs act, from federal largesse, are icing on the cake. I do consider that Intel will derive some payoff from each, and I’m shopping for Intel, to twin with what’s left of my Nvidia funding from six years in the past.

- Walgreens: For Walgreens, the choices are dwindling, as its core companies face challenges. That stated, and even with its retailer closures, Walgreens stays the second largest drugstore chain in america, after CVS. Shrinking its presence to its most efficient shops and shedding the remainder stands out as the pathway to survival, however the firm must determine a option to carry down its debt proportionately. There’s the danger {that a} macro slowdown or a capital market shock, inflicting default threat and spreads to widen, might wipe out fairness buyers. With all of that stated, and constructing in a threat of failure to the evaluation, I estimated the worth per share underneath totally different development and profitability assumptions: The valuation pivots fully on whether or not working margins enhance to historic ranges, with margins of 4% or greater translating into values per share that exceed the inventory value. I consider that the pharmacy enterprise is ripe for disruption, and that the margins won’t revert again to pre-2021 ranges, making Walgreens a “no go” for me.

- Starbucks: Starbucks is the outlier among the many three firms, insofar as its income development remains to be strong and it stays a money-making agency. Its largest drawback is that it has misplaced its story line, and it must rediscover a story that may not solely give buyers a way of the place it’s going, however will redirect how it’s managed. As I famous in my submit on company life cycle, story telling requires visionaries, and within the case of Starbucks, that visionary additionally has to know the logistical challenges of operating espresso outlets. I have no idea sufficient about Brian Niccol to find out whether or not he matches the invoice. As somebody who led Taco Bell and Chipotle, I believe that he can get the second half (understanding restaurant logistics) nailed down, however is he a visionary? He is perhaps, however visionary CEOs typically don’t dwell a thousand miles from company headquarters, and fly company jets to work half time at their jobs, and Niccol has supplied no sense of what he sees as the brand new Starbucks narrative but. For the second, thought, there appears to be euphoria available in the market that change is coming, although nobody appears clear on what that change is, and the inventory value has virtually totally recovered from its swoon to succeed in $91 on September 8, 2024. That value is nicely above any worth per share that I can get for the corporate, even assuming that they return to historic norms:

I have to be lacking a few of the Starbucks magic that buyers are seeing, since there is no such thing as a mixture of historic development/margins that will get me near the present inventory value. Actually, the one approach my worth per share reaches present pricing ranges is that if I see the corporate sustaining its income development charges from 2002-2011, whereas delivering the a lot greater working margins that it earned between 2012-2021. That, to me, is a bridge too far to cross.

The Endgame

There’s a motive that so many individuals wish to be entrepreneurs and begin new companies. However the excessive mortality charge, constructing a brand new enterprise is thrilling and, if profitable, vastly rewarding. A wholesome economic system will encourage entrepreneurship, offering threat capital and never tilting the enjoying subject in the direction of established gamers; it stays the strongest benefit that america has over a lot of the remainder of the world. Nevertheless, additionally it is true that the measure of a wholesome economic system is in the way it offers with declining companies and companies. If as Joseph Schumpeter put it, capitalism is all about inventive destruction, it follows that firms, that are in spite of everything authorized entities that function companies, ought to fade away as the explanations for his or her existence fade. That’s one motive I critique your complete notion of company sustainability (versus planet sustainability), since conserving declining firms alive, and supplying them with further capital, redirects that capital away from companies that would do much more good (for the economic system and society) with that capital.

If there’s a subtext to this submit, it’s that we want a more healthy framing of company decline, as inevitable in any respect companies, throughout their life cycle, somewhat than one thing that ought to be fought. In enterprise faculties and books, we have to spotlight not simply the empire builders and the corporate saviors, i.e., CEOs who rescued failing firms and made their firms greater, however the empire shrinkers, i.e., CEOs who’re introduced into declining companies, who preside over an orderly (and worth including) shrinkage or breaking of their companies. In investing, it’s true that the glory will get reserved for the Magazine Seven and the FANGAM shares, firms that appear to have discovered the magic to continue to grow at the same time as they scale up, however we also needs to take note of firms that discover their option to ship worth for shareholders in unhealthy companies.

YouTube Video

Hyperlinks

Valuations