My different publish listed 2024 2025 401k and IRA contribution and earnings limits. I additionally calculated the inflation-adjusted tax brackets and a number of the mostly used numbers in tax planning for 2025 utilizing the printed inflation numbers and the identical components prescribed within the tax regulation.

2024 2025 Commonplace Deduction

You don’t pay federal earnings tax on each greenback of your earnings. You deduct an quantity out of your earnings earlier than you calculate taxes. About 90% of all taxpayers take the usual deduction. The opposite ~10% itemize deductions when their complete deductions exceed the usual deduction. In different phrases, you’re deducting a bigger quantity than your allowed deductions whenever you take the usual deduction. Don’t really feel unhealthy about taking the usual deduction!

The essential normal deduction in 2024 and my estimate for 2025 are:

| 2024 | 2025 estimates | |

|---|---|---|

| Single or Married Submitting Individually | $14,600 | $15,050 |

| Head of Family | $21,900 | $22,550 |

| Married Submitting Collectively | $29,200 | $30,100 |

Supply: IRS Rev. Proc. 2023-34, creator’s calculations.

People who find themselves age 65 and over have the next normal deduction than the fundamental normal deduction.

| 2024 | 2025 estimates | |

|---|---|---|

| Single, age 65 and over | $16,550 | $17,050 |

| Head of Family, age 65 and over | $23,850 | $24,550 |

| Married Submitting Collectively, one individual age 65 and over | $30,750 | $31,700 |

| Married Submitting Collectively, each age 65 and over | $32,300 | $33,300 |

Supply: IRS Rev. Proc. 2023-34, creator’s calculations.

People who find themselves blind have an extra normal deduction.

| 2024 | 2025 estimates | |

|---|---|---|

| Single or Head of Family, blind | +$1,950 | +$2,000 |

| Married Submitting Collectively, one individual is blind | +$1,550 | +$1,600 |

| Married Submitting Collectively, each are blind | +$3,100 | +$3,200 |

Supply: IRS Rev. Proc. 2023-34, creator’s calculations.

2024 2025 Tax Brackets

The tax brackets are based mostly on taxable earnings, which is AGI minus numerous deductions. The tax brackets in 2024 are:

| Single | Head of Family | Married Submitting Collectively | |

|---|---|---|---|

| 10% | $0 – $11,600 | $0 – $16,550 | $0 – $23,200 |

| 12% | $11,600 – $47,150 | $16,550 – $63,100 | $23,200 – $94,300 |

| 22% | $47,150 – $100,525 | $63,100 – $100,500 | $94,300 – $201,050 |

| 24% | $100,525 – $191,950 | $100,500 – $191,950 | $201,050 – $383,900 |

| 32% | $191,950 – $243,725 | $191,950 – $243,700 | $383,900 – $487,450 |

| 35% | $243,725 – $609,350 | $243,700 – $609,350 | $487,450 – $731,200 |

| 37% | Over $609,350 | Over $609,350 | Over $731,200 |

Supply: IRS Rev. Proc. 2023-34.

My estimated 2025 tax brackets are:

| Single | Head of Family | Married Submitting Collectively | |

|---|---|---|---|

| 10% | $0 – $11,950 | $0 – $17,050 | $0 – $23,900 |

| 12% | $11,950 – $48,550 | $17,050 – $64,950 | $23,900 – $97,100 |

| 22% | $48,550 – $103,500 | $64,950 – $103,500 | $97,100 – $207,000 |

| 24% | $103,500 – $197,600 | $103,500 – $197,600 | $207,000 – $395,200 |

| 32% | $197,600 – $250,925 | $197,600 – $250,900 | $395,200 – $501,850 |

| 35% | $250,925 – $627,300 | $250,900 – $627,300 | $501,850 – $752,750 |

| 37% | Over $627,300 | Over $627,300 | Over $752,750 |

Supply: creator’s calculations.

A standard false impression is that whenever you get into the next tax bracket, all of your earnings is taxed on the greater charge and also you’re higher off not having the additional earnings. That’s not true. Tax brackets work incrementally. For those who’re $1,000 into the following tax bracket, solely $1,000 is taxed on the greater charge. It doesn’t have an effect on the earnings within the earlier brackets.

For instance, somebody single with a $70,000 AGI in 2024 can pay:

| First 14,600 (the usual deduction) | 0% | ||

| Subsequent $11,600 | 10% | ||

| Subsequent $35,550 ($47,150 – $11,600) | 12% | ||

| Remaining $8,250 | 22% |

This individual is within the 22% tax bracket however solely a tiny fraction of the $70,000 AGI is taxed at 22%. A lot of the earnings is taxed at 0%, 10%, and 12%. The blended tax charge is barely 10.3%. If this individual doesn’t earn the ultimate $8,250, she or he is within the 12% bracket as a substitute of the 22% bracket however the blended tax charge solely goes down barely from 10.3% to eight.8%. Making the additional earnings doesn’t price this individual extra in taxes than the additional earnings.

Don’t be afraid of going into the following tax bracket.

2024 2025 Capital Good points Tax

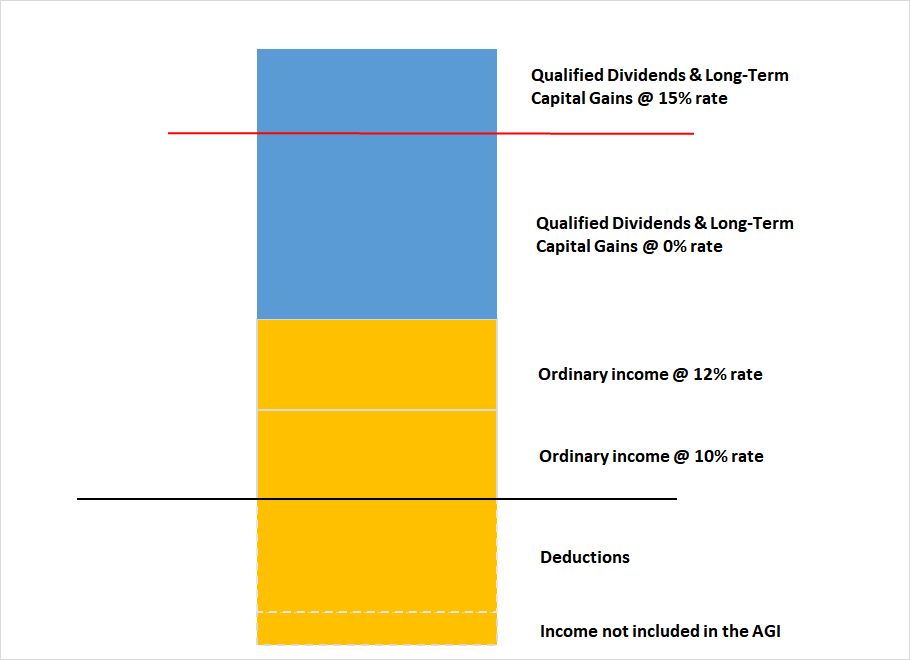

When your different taxable earnings (after deductions) plus your certified dividends and long-term capital beneficial properties are under a cutoff, you’ll pay 0% federal earnings tax in your certified dividends and long-term capital beneficial properties beneath this cutoff.

That is illustrated by the chart under. Taxable earnings is the half above the black line, after subtracting deductions. A portion of the certified dividends and long-term capital beneficial properties is taxed at 0% when the opposite taxable earnings plus these certified dividends and long-term capital beneficial properties are beneath the pink line.

The pink line is near the highest of the 12% tax bracket however they don’t line up precisely.

| 2024 | 2025 estimates | |

|---|---|---|

| Single or Married Submitting Individually | $47,025 | $48,425 |

| Head of Family | $63,000 | $64,850 |

| Married Submitting Collectively | $94,050 | $96,850 |

Supply: IRS Rev. Proc. 2023-34, creator’s calculations.

For instance, suppose a married couple submitting collectively has $70,000 in different taxable earnings (after deductions) and $25,000 in certified dividends and long-term capital beneficial properties in 2024. The utmost zero charge quantity cutoff is $94,050. $24,050 of the certified dividends and long-term capital beneficial properties ($94,050 – $70,000) is taxed at 0%. The remaining $25,000 – $24,050 = $950 is taxed at 15%

An identical threshold exists on the higher finish for certified dividends and long-term capital beneficial properties. When your different taxable earnings (after deductions) plus your certified dividends and long-term capital beneficial properties are above a cutoff, you’ll pay 20% federal earnings tax as a substitute of 15% in your certified dividends and long-term capital beneficial properties above this cutoff.

| 2024 | 2025 estimates | |

|---|---|---|

| Single | $518,900 | $534,200 |

| Head of Family | $551,350 | $567,550 |

| Married Submitting Collectively | $583,750 | $600,950 |

| Married Submitting Individually | $291,850 | $300,475 |

Supply: IRSRev. Proc. 2023-34, creator’s calculations.

Internet Funding Revenue Tax

Internet Funding Revenue Tax (NIIT) is a 3.8% tax on the portion of curiosity, dividends, and capital beneficial properties that makes your modified adjustable gross earnings exceed these thresholds:

| MAGI Threshold | |

|---|---|

| Single | $200,000 |

| Head of Family | $200,000 |

| Married Submitting Collectively | $250,000 |

| Married Submitting Individually | $125,000 |

These thresholds are mounted by regulation. They aren’t adjusted for inflation. You pay 3.8% tax on the quantity your MAGI exceeds these thresholds or your complete curiosity, dividends, and capital beneficial properties, whichever is much less.

Suppose you’re married submitting collectively and you’ve got $300,000 MAGI, which incorporates $10,000 in curiosity, dividends, and capital beneficial properties. Though your MAGI exceeds the $250,000 threshold by $50,000, you’ll pay 3.8% in NIIT on solely $10,000 as a result of you have got solely $10,000 in internet funding earnings.

Suppose you’re married submitting collectively and you’ve got $260,000 MAGI, which incorporates $150,000 in curiosity, dividends, and capital beneficial properties. Though you have got $150,000 in internet funding earnings, you’ll pay 3.8% in NIIT solely on $10,000 as a result of your MAGI exceeds the $250,000 threshold by solely $10,000.

2024 2025 Property and Belief Tax Brackets

Estates and trusts have totally different tax brackets than people. These apply to non-grantor trusts and estates that retain earnings versus distributing the earnings to beneficiaries. Grantor trusts (together with the most typical revocable residing trusts) don’t pay taxes individually. The earnings of a grantor belief is taxed to the grantor on the grantor’s tax brackets.

Listed below are the tax brackets for estates and trusts in 2024 and my estimates for 2025:

| 2024 | 2025 estimates | |

|---|---|---|

| 10% | $0 – $3,100 | $0 – $3,150 |

| 24% | $3,100 – $11,150 | $3,150 – $11,450 |

| 35% | $11,150 – $15,200 | $11,450 – $15,650 |

| 37% | over $15,200 | over $15,650 |

Supply: IRS Rev. Proc. 2023-34, creator’s calculations.

2024 2025 Certified Charitable Distributions (QCD) Restrict

Folks older than 70-1/2 could make Certified Charitable Distributions (QCD) from their Conventional IRA on to qualifying charitable organizations. QCDs depend towards the Required Minimal Distribution (RMD).

Your complete QCDs can’t exceed $105,000 in 2024. I estimate the restrict will go as much as $108,000 in 2025.

The QCD restrict is per individual. For those who’re married, each you and your partner could make QCDs as much as the restrict individually out of your respective IRAs.

Supply: IRS Discover 2023-75, creator’s calculations.

2024 2025 2026 Medicare Half B and Half D IRMAA

Folks on Medicare Half B and Half D pay the next Medicare premium when their Modified Adjusted Gross Revenue from two years in the past crosses sure thresholds. I observe these in Medicare Half B IRMAA Premium MAGI Brackets.

2024 2025 Present Tax Exclusion

Every individual can provide one other individual as much as a set quantity in a calendar 12 months with out having to file a present tax type. Not that submitting a present tax type is onerous, however many individuals keep away from it if they will. This present tax exclusion quantity will enhance from $18,000 in 2024 to $19,000 in 2025.

| 2024 | 2025 estimate | |

|---|---|---|

| Present Tax Exclusion | $18,000 | $19,000 |

Supply: IRS Rev. Proc. 2023-34, creator’s calculations.

The present tax exclusion is counted by every giver to every recipient. As a giver, you can provide as much as $18,000 every in 2024 to a vast variety of individuals with out having to file a present tax type. For those who give $18,000 to every of your 10 grandkids in 2024, you continue to received’t be required to file a present tax type. Any recipient may obtain a present from a vast variety of individuals. If a grandchild receives $18,000 from every of his or her 4 grandparents in 2024, no taxes or tax varieties will probably be required.

2024 2025 Financial savings Bonds Tax-Free Redemption for Faculty Bills

For those who money out U.S. Financial savings Bonds (Sequence I or Sequence EE) for school bills or switch to a 529 plan, your modified adjusted gross earnings have to be beneath sure limits to get a tax exemption on the curiosity. See Money Out I Bonds Tax Free For Faculty Bills Or 529 Plan.

Listed below are the earnings limits in 2024 and my estimates for 2025. The boundaries are in a phase-out vary. You get a full exemption in case your earnings is under the decrease quantity within the vary. You get no exemption in case your earnings is above the upper quantity within the vary. You get a partial exemption in case your earnings falls throughout the vary.

| 2024 | 2025 estimates | |

|---|---|---|

| Single, Head of Family | $96,800 – $111,800 | $99,650 – $114,650 |

| Married Submitting Collectively | $145,200 – $175,200 | $149,500 – $179,500 |

Supply: IRS Rev. Proc. 2023-34, creator’s calculations.

Say No To Administration Charges

In case you are paying an advisor a share of your belongings, you might be paying 5-10x an excessive amount of. Learn to discover an unbiased advisor, pay for recommendation, and solely the recommendation.