It has been an unsettling summer time for anybody with a stake within the film, tv and broadcasting companies. The strike by display screen actors and writers which began in July is now into nearly into its third month, endlessly, placing in danger the pipeline of flicks and reveals that have been anticipated to hit theaters and streaming platforms within the subsequent few months. On August 31, Disney pulled its tv channels from Spectrum (owned by Constitution, the second largest cable firm within the US, after Comcast) after a dispute about funds for carrying these channels. Tennis followers, on the brink of watch the US Open on ESPN, have been apoplectic, as their televisions went clean in the course of matches, and Disney, along with encouraging them to complain to Spectrum, supplied them an choice of switching to Hulu+ Dwell TV, a streaming service various to cable. Whereas actors and writers have been on strike earlier than, and contractual disputes between content material makers and cable suppliers is par for the course, the information tales of this summer time appear extra consequential, maybe as a result of they replicate longer time shifts within the film and broadcasting companies.

Talking of Disney, an organization that has discovered itself within the crosshairs of political and cultural disputes, the inventory hit $80 on September 7, near a ten-year low. So as to add to the angst, the specter of synthetic intelligence (AI) overhangs nearly each side of the enterprise, and is likely one of the contested points within the strike. The current troubles in leisure, although, replicate a long run disruption that has occurred within the enterprise, with the rise of streaming as a substitute for the normal platforms for motion pictures and tv reveals. On this publish, I’ll give attention to how streaming has not solely modified the best way we devour content material, however has additionally modified the best way that content material will get made. Within the course of, it has altered the monetary traits of the businesses within the enterprise in ways in which the market continues to be attempting to return to phrases with, which can clarify the market turmoil this yr.

A Cautionary Story: The Music Enterprise and Streaming

If, as you watch the broadcasting enterprise undergo its struggles with streamers, you get a way of deja vu, it’s as a result of the music enterprise within the Nineties discovered itself equally challenged, and its upending by streaming might supply classes for the film enterprise. Within the twentieth century, the music enterprise adopted a well-honed script. It was composed of corporations which scouted for music expertise, signed these musicians to music label contracts after which labored with them of their studios to provide report albums that have been bought in music shops throughout the nation. The music corporations supplied advertising and marketing assist, looking for out radio stations that may carry their music, and distributional backing to get albums to retailers. In some ways, it was unattainable for a musician to interrupt via, with out studio backing, and that energy imbalance allowed the latter to assert the lion’s share of the revenues.

The disruptor who upset the music enterprise was Napster, a platform that delivered pirated streams of music to its prospects, successfully undercutting the necessity to enter music shops and purchase costly albums. Whereas Napster downloads left a lot to be desired by way of audio high quality, and the corporate walked to (and infrequently past) the very fringe of legality, it uncovered the weaknesses within the music enterprise, from how new artists have been discovered and marketed, to how their music was packaged and at last, how that music was bought. When the music corporations of the day have been capable of shut Napster down in 2001, citing digital piracy, they have been undoubtedly relieved, however their weaknesses had been uncovered. Apple created the iTunes Retailer in 2001, permitting prospects to purchase particular person songs, moderately than whole albums, and the unbundling of the music enterprise started. Within the years that adopted, music albums and music retailers turned rarer, and the appearance of the web allowed musicians to bypass the gatekeepers on the music studios and go on to prospects. As good telephones and private units turned extra plentiful, Spotify and Pandora launched the music streaming mannequin, and the sport was perpetually modified, and the results for the music enterprise have been staggering:

-

The music enterprise shrank and the middle of gravity shifted: The entry of streaming corporations modified the economics of music, because it largely eliminated the necessity to purchase music, even within the single-song format. Spotifyand Pandora allowed subscribers entry to immense music libraries, with excessive audio high quality, and as they grew, revenues to present music labels dropped:

As you may see, music revenues shifted (unsurprisingly) from studios to music streaming, however in a extra troubling signal, the mixture revenues of the music enterprise dropped by nearly 40% between 2000 and 2016. On a extra optimistic be aware, the revenues are actually again to pre-2000 ranges, albeit not on inflation-adjusted foundation, and 65% of all revenues in 2021 got here from streaming. It’s simple that streaming, by eradicating most of the intermediaries within the previous music enterprise mannequin, has shrunk the enterprise.

- The established order crumbled: As revenues shrunk, and moved from the studios to the streamers, the businesses that represented the established order imploded. The music studio enterprise, which had a dozen or extra energetic gamers within the final century, has consolidated right into a handful of corporations, most of that are small components of a lot larger leisure corporations (Sony. Vivendi), and most of the largest labels in music (Abbey Roads, Motown) are historic artifacts which have bought their music rights to others. The music retail enterprise was decimated, as music retailers like Tower Information shut down, and as artists seeking to change misplaced revenues from report gross sales with reside performances and merchandising gross sales, corporations like LiveNation stepped in to fill the necessity.

- The divergence in musician take turned bigger: As revenues shrunk and partially recovered, not all musicians have shared within the new pie equally. The highest one % of musicians account for ninety % of all music streams and near sixty % of revenues from concert events. A enterprise that has at all times been prime heavy by way of rewarding success, has change into much more so.

- Personalities turned larger than music labels: The appearance of social media has allowed the best profile performers to interrupt freed from a lot of the intermediaries within the music enterprise. When you’re Beyonce, and you’ve got 15.3 million followers on Twitter and 317 million followers in Instagram, you may have extra attain and persuasive powers than any music firm on the face of the earth. Whereas it’s true that social media has allowed just a few musicians to interrupt via and change into successes, I feel it’s simple that social media is exacerbating the variations between large identify musicians and unknowns greater than it’s serving to shut the hole.

As film and broadcast enterprise executives look over their shoulders at what streaming has in retailer for them, just a few of them are undoubtedly trying on the implosion of the music enterprise and questioning whether or not an identical destiny awaits them. The extra optimistic amongst them will level to variations between the music and film companies that can make the latter extra resilient, however the extra pessimistic will be aware the similarities. To place it in additional existential phrases, if the film enterprise resembles the music enterprise in the way it responds to streaming, there’s a boatload of ache that’s coming for the established order, with the important thing distinction being {that a} meltdown just like the one seen in music will wipe out a whole lot of billions of {dollars} in worth, moderately than the tens of billions within the music enterprise.

Film and Broadcasting – The Twentieth Century Lead In

The film enterprise had its beginnings within the early 1900s, when the primary motion pictures have been made and Hollywood turned the vacation spot of selection for film makers, no less than in the USA. Within the years after, the nice film studios had their beginnings, with the precursor to Paramount being created by Cecil B. DeMille and others in 1915, adopted quickly by Metro Goldwyn Mayer (MGM), RKO, twentieth Century Fox and Warner Bros (creating the Massive 5), in addition to by smaller gamers (Common, United, Columbia), . Within the golden age (no less than for the studios), these 5 studios managed nearly each side of the flicks, together with content material, distribution and exhibition, with film actors successfully owned and managed by the studios that found them. It took the US Supreme Courtroom and use of the anti-trust legislation, in 1948, to first pressure studios out of the movie show possession enterprise, after which to launch film stars from their bondage, and within the course of, it ended the Studio Age.

Pressured to divest themselves of film theaters and of their management of film stars, the studios have been capable of offset the negatives with the positives from new applied sciences (Technicolor, stereo sound) and an nearly unchallenged declare on American leisure time, with near two-thirds of People going to the flicks no less than as soon as every week within the Nineteen Fifties. Within the Nineteen Seventies, Hollywood found the payoff from blockbuster motion pictures, and the film enterprise turned more and more depending on the most important blockbusters delivering sufficient revenues and income to cowl a complete host of flicks that both misplaced cash or broke even. Whereas Jaws and the primary three Star Wars motion pictures (A New Hope, The Empire Strikes Again, The Return of the Jedi) weren’t the primary mega-hits in historical past, they accelerated the pattern in the direction of the blockbuster phenomenon that continues via at this time. Within the Eighties, the start of video gamers created methods for studios to complement revenues at film theaters with revenues from promoting movies and DVDs, whereas opening the door to unlawful copying and piracy.

By means of this era, the large studios nonetheless managed a big share of the content material enterprise, however unbiased research, usually extra daring in selection of matters and settings, took a share. That mentioned, the film enterprise remained concentrated, with the most important gamers dominating every phase of the enterprise.

That film enterprise was constructed round field workplace receipts at film theaters, cut up between the film makers and the theater house owners. The latter have been capital intensive, since they occupied helpful actual property, owned or leased by the theater corporations. Although the theater-owners have been nominally unbiased, studios retained important bargaining energy with these exhibitors and the sharing of supplemental revenues.

The broadcasting enterprise lagged the film enterprise, by way of growth, as a result of televisions didn’t begin making their approach into households in ample numbers till the Nineteen Fifties, but it surely too was constructed round a system of content-production, distribution and exhibition, however with promoting on the coronary heart of its income era. The dominance of the three large networks (ABC, CBS and NBC) in tv viewing meant that tv reveals needed to attain the broadest potential audiences to achieve success, and television present success was measured with (Nielsen) rankings, measuring how a lot they have been watched, and a complete enterprise was constructed round these measurements. That enterprise was disrupted within the Nineteen Seventies and Eighties with the arrival of cable tv, and cable’s capability to hold a whole lot of channels, a few of which catered to area of interest markets, shaking the main community maintain on viewers and altering content material once more. In the beginning of 2010, it was estimated that near 75% of all US households obtained their tv via a cable or satellite tv for pc supplier, setting the stage for the following large disruption within the enterprise.

Film and Broadcasting: The Streaming Period

Netflix, which is now synonymous with the streaming menace to motion pictures, began its life as a video rental firm, extra of a menace to Blockbuster video, the lead participant in that enterprise, than to any of the bigger gamers within the content material enterprise. It’s price remembering that Netflix entree into the enterprise was initially on the US postal system, with the innovation being that you possibly can have the movies you needed to observe mailed to you, as a substitute of going right into a video rental retailer. Because the capability of the web to ship massive information improved, Netflix shifted to digital distribution, albeit with angst on the a part of some present prospects, but it surely nonetheless relied totally on rented content material (from the normal studios). It was in response to being squeezed by the studios on funds for this content material that Netflix determined to attempt its hand at unique content material, with Home of Playing cards and Orange is the brand new Black representing their first main forays, and set in sequence the occasions which have led us to the place we stand at this time.

The Netflix Disruption

The rise of Netflix as a streaming big has been meteoric, and it may be seen each within the progress in subscribers and revenues on the firm, particularly within the final decade.

Embedded in these numbers are two different tendencies price noting. The primary is that the % of content material that Netflix produced (unique content material) elevated from nearly nothing in 2011 to shut to 50% of content material in 2022. The second is that progress lately, in subscribers and revenues, has come from outdoors the US, with US declining from 52% of all subscribers in 2018 to 33.6% of subscribers in 2022.

As Netflix has grown, it has drawn competitors not solely from conventional content material makers, with the biggest studios providing their very own streaming providers (Disney -> Disney +, Paramount -> Paramount+ & Showtime, Warner -> (HBO) Max, Common -:> Peacock, MGM -> MGM+), but in addition from massive know-how corporations (Apple TV+ and Amazon Prime). Whereas Netflix stays probably the most watched streaming service, many shoppers subscribe to a number of streaming providers, and as streaming selections proliferate, increasingly US households have began weaning themselves away from cable TV. This twine reducing phenomenon’s results might be seen in the % of households that haven’t any cable or satellite tv for pc TV:

As streaming has breached the broadcasting enterprise, you might marvel how it’s affecting the film enterprise. Within the early years, streaming allowed studios to enhance the worth of their content material by renting it out to streamers (Netflix, specifically) for substantial revenues. As its subscription base grew, Netflix turned to creating unique motion pictures, largely for its personal platform, and in 2019, it spent near $15 billion on unique content material, rivaling the spending of enormous film makers.

The Streaming Impact

As streaming disrupts each the broadcasting and film companies, allow us to take a look at how it’s altering these companies from the within, beginning with content material (varieties of motion pictures, film budgets, variety of motion pictures), shifting on to expertise (actor and author demand and compensation) after which to prospects (how a lot and the way we watch content material).

Content material

The expansion of streaming platforms has altered content material (motion pictures and broadcasting) in important methods., with the primary being an improve within the complete quantity of content material, as streaming platforms attempt to fill their content material libraries. With Netflix main the best way on unique content material, this has translated right into a bounce in motion pictures being made, as might be seen within the graph beneath, from an annual common of 367 motion pictures a yr, in the USA, between 2000 and 2012 to 1200 motion pictures a yr between 2013 and 2023.

That improve in demand for content material has been accompanied by an improve in prices of film making, with the typical price for making a film growing from $39.5 million between 2000 and 2012 to about $54.5 million between 2013 and 2023.

In case you are questioning why you haven’t seen an explosion of flicks at theaters, it’s as a result of fewer of those motion pictures are being made for film theaters, with large studios, decreasing theater film manufacturing by nearly 30%, from 108 motion pictures a yr, on common from 2000 to 2012, to about 75 motion pictures a yr, from 2013 to 2023. Whereas unbiased research elevated their manufacturing over the interval, the general variety of motion pictures reaching film theaters has seen a major drop off.

Whereas the 2020 drop might be attributed to the shut down, film manufacturing has not bounced again within the years since.

Lastly, the most fascinating results of streaming could also be occurring below the floor by way of the content material that’s produced, and they are often traced to the very totally different economics of creating motion pictures for theaters (or reveals for broadcasting) versus creating content material for streaming providers. With the previous, the query of whether or not to make content material might be answered by forecasting the revenues that will likely be generated by that content material, both as gate receipts and ancillary revenues (for motion pictures) or in promoting revenues (for broadcasting). With streaming, the top sport with new content material (motion pictures or reveals) is so as to add new subscribers to the service, and/or induce present subscribers to resume their subscriptions, and it’s troublesome to hyperlink both on to particular person reveals. Even inside streaming providers, there appears to be no consensus on what technique greatest delivers these outcomes, maybe as a result of success is so troublesome to measure.

- Netflix has chosen what might be greatest described because the shotgun method to content material, producing huge quantities of content material, usually within the type of whole seasons, for reveals, with the hope that some portion of that content material can be a binge-watching hit. That method has delivered outcomes by way of increased subscriber rely, however at an enormous content material price, with content material prices rising on the similar price, or increased charges, than subscriber rely, till very just lately.

- HBO has used a extra curated method to content material, making fewer reveals, albeit with much less divergence in high quality, and releasing episodes on a weekly foundation, hoping for extra viral attain from profitable reveals (Sport of Thrones and Succession qualify as large successes). The plus of this method is decrease content material prices, however with a lot decrease subscriber numbers than within the shotgun mannequin.

- Disney Plus began with the premise {that a} huge library of content material would permit the platform to attract and hold subscribers, however early on, the corporate found that to compete with Netflix on subscriber numbers, it wanted new content material, and far of that content material has come from high-profile, costly reveals from its Avengers and Star Wars franchises. If success is measured in subscriber rely, Disney Plus has succeeded, however the spending on content material has exploded, dragging Disney’s profitability down with it.

- With Apple TV+ and Amazon Prime, the sport is much more troublesome to gauge. Each corporations spend massive quantities in content material and clearly lose cash on their streaming platforms, however their advantages might come from tying customers extra intently into their platforms. with advantages displaying up different services and products they promote to these of their ecosystems.

Given that every one of those approaches have had troublesome delivering sustained profitability, it’s truthful to say that whereas streaming has succeeded in delivering subscriber progress and altering content material watching habits, it has not developed a enterprise mannequin that may delivered sustained profitability.

Expertise

The angst that many actors and writers in regards to the sharing of streaming revenues might be greatest understood by contemplating how how they’ve traditionally obtained residual funds on content material. Constructed round a pay construction negotiated in 1960, actors and writers are paid residuals every time a present runs on broadcast or cable TV, or when somebody buys a DVD or videotape of the present. With streaming, that previous construction has buckled, as the advantages from a present or film are tougher to measure, since subscription income or subscriber rely can’t be instantly linked to particular person reveals. (There are exceptions, the place added subscriber numbers might be attributed to successful present, say Sport of Thrones at HBO, or perhaps a high-profile particular person, with Lionel Messi pushing up MLS subscriptions on Apple TV+.) To the counter which you can measure how many individuals watch a present or film on Netflix or Disney+, be aware that streaming corporations don’t become profitable from viewers, however solely from added subscription revenues. With the extra diffuse hyperlink between viewership and revenues in streaming, the query of the right way to construction residuals to actors and writers has change into a key level of rivalry, and one of many central parts of the present strike.

In 2019, the Display screen Actors Guild made an settlement with Netflix that utilized to any scripted initiatives produced and distributed by the platform the place residuals have been calculated based mostly on the quantity {that a} performer was initially paid and what number of subscribers the streaming platform has. That settlement although has yielded wildly divergent funds to actors, with some taking to social media to showcase how little they obtained, even on extensively watched reveals, whereas different larger identify stars are being properly compensated. One of many calls for from strikers is that streaming providers be extra clear about viewership on reveals and that they tie compensation extra intently to viewership, however this dispute won’t be simply resolved. Given the stakes, an settlement will ultimately be reached the place actors and writers will obtain greater than what they’re receiving now, however to the extent that streaming will get its worth from including and holding on to subscribers, I count on the divergence in pay between the celebs of streaming reveals and the remainder of the content material makers to worsen over time, simply because it did within the music enterprise.

Consumption

Has streaming modified the best way that we watch motion pictures and broadcasting content material? I feel so, and listed below are just a few generalizations about these viewing adjustments:

- Extra selection, however much less high quality management: The truth that Netflix has constructed its content material manufacturing across the shotgun method, and is being copied by different streamers, you and I as shoppers will likely be spending much more time beginning and abandoning reveals, earlier than discovering ones to observe than we used to. Not surprisingly, fairly just a few us are overwhelmed by that seek for watchable content material, and select to go along with the acquainted (explaining the success of previous community reveals like The Workplace, Buddies and Fits on Netflix) or with the herd, usually watching what everybody else is watching (the ten most watched reveals and films that Netflix highlights day by day create suggestions loops that cause them to be watched extra).

- Copycat Productions: The content material enterprise have by no means been shy about imitation and sequels, attempting to remake profitable content material with slight variations or add sequels to hits, however that has notched up with streaming. Thus, the success of a present on Netflix provides rise not solely to extra seasons of that present, however to a complete host of imitations. When you add to this the truth that streaming platforms monitor what you watch, and have algorithms that feed you extra of the identical, you might very properly have the misfortune of being caught in a model of Groundhog Day, the place you watch the identical film, with gentle variations, time and again for the remainder of your life.

- YouTube and TikTok: Because the content material on streaming platforms dilutes high quality and shifts to actuality reveals, it ought to come as no shock that viewers are spending much less time on streaming platforms and extra on Twitch, YouTube and TikTok, the place you get to observe individuals put out actuality reveals of their very own, typically in actual time.

Lastly, the early promise of streaming was that it might permit us to economize, by reducing the cable twine, however as with most issues that know-how has promised us, these monetary financial savings have change into a mirage. When you add collectively the price of a number of streaming providers to the upper worth that you simply paid to get higher-spreed broadband, to observe your streaming reveals, I’m positive that a lot of you’re paying extra in your leisure funds than you probably did in pre-streaming days.

The Streaming Impact: Enterprise Fashions and Profitability

The consequences of streaming on motion pictures and broadcasting content material and distribution are displaying up within the monetary statements of those corporations and available in the market pricing of those corporations. On this part, I’ll begin by how the working metrics of leisure corporations, with the intent of detecting shifts in progress and profitability, after which flip my consideration to how traders are pricing in these adjustments.

Working Results

For individuals who are involved a couple of music business-like implosion in film enterprise revenues, I’ll begin with the excellent news. Not less than up to now, the cumulative revenues throughout all leisure corporations c has held as much as the streaming disruption, as might be seen within the graph beneath, the place I take a look at the cumulative revenues of all film and broadcasting associated corporations from 1998 to 2023:

Notice that since corporations are labeled based mostly upon their core enterprise on this graph, the streaming element of revenues are understated, because the revenues that Disney, Paramount and Warner get from their streaming companies are counted as film revenues. As you may, mixture revenues did see a drop in 2020, due to COVID, however have come again since. In case you are questioning why cable firm revenues have been resilient within the face of twine reducing and the lack of cable TV subscriptions, it’s as a result of cable corporations stay the prime suppliers of broadband, with out which there is no such thing as a streaming enterprise.

On a much less upbeat be aware, profitability at these corporations, the cumulative working income have been much less reselient, particularly within the post-COVID years, with cumulative working income in 2022 and 2023 properly beneath working income in 2019:

When you carry the revenues and working numbers collectively to compute working margins, you begin to get a clearer sense of why film corporations, specifically, are dealing with a disaster:

The profitability of the film enterprise has collapsed within the years since COVID, with working margins dropping beneath 5% in 2022 and 2023, from greater than 15% within the years earlier than COVID. Streaming appears to be settling right into a modicum of profitability, however right here once more, we could also be overstating the profitability of streaming by not bringing into the metric the losses that Disney, Warner Bros and Paramount are dealing with on their streaming segments.

In sum, leisure corporations are delivering increased revenues general, with revenues from streaming and new applied sciences growing sufficient to offset misplaced revenues in legacy companies which are being disrupted, however the leisure enterprise general is turning into much less worthwhile.

Market Results

As streaming has modified the film and broadcasting companies, monetary markets have struggled to get a deal with on how these adjustments have an effect on the values of corporations int these companies. Wanting on the cumulative market capitalization of all leisure corporations, there are two shifts that we will observe over time, one within the decade main into COVID and one within the years after:

Notice the surge in mixture market capitalization between 2019 and 2021, with Netflix main the best way, and with different leisure corporations partaking, and the drop in worth within the final two years. The tendencies in cumulative market capitalization of all leisure corporations additionally masks shifts in worth throughout corporations inside the group, as might be seen within the graph beneath, the place I take a look at the diverging fortunes throughout the final decade of the 5 largest leisure corporations (by way of market capitalization) in September 2023:

Between 2013 and September 2023, Netflix gained $174 billion in market capitalization, posting an annual return of 24.5% a yr. Throughout the identical interval, Comcast, Disney and Warner noticed their market capitalizations stagnate, in a interval when the market was up strongly, successfully translating right into a misplaced decade of returns to shareholders. Dwell Nation, the fifth largest firm within the group in September 2023, barely registered within the rankings in 2013, however has risen 17.19% a yr to succeed in its present standing.

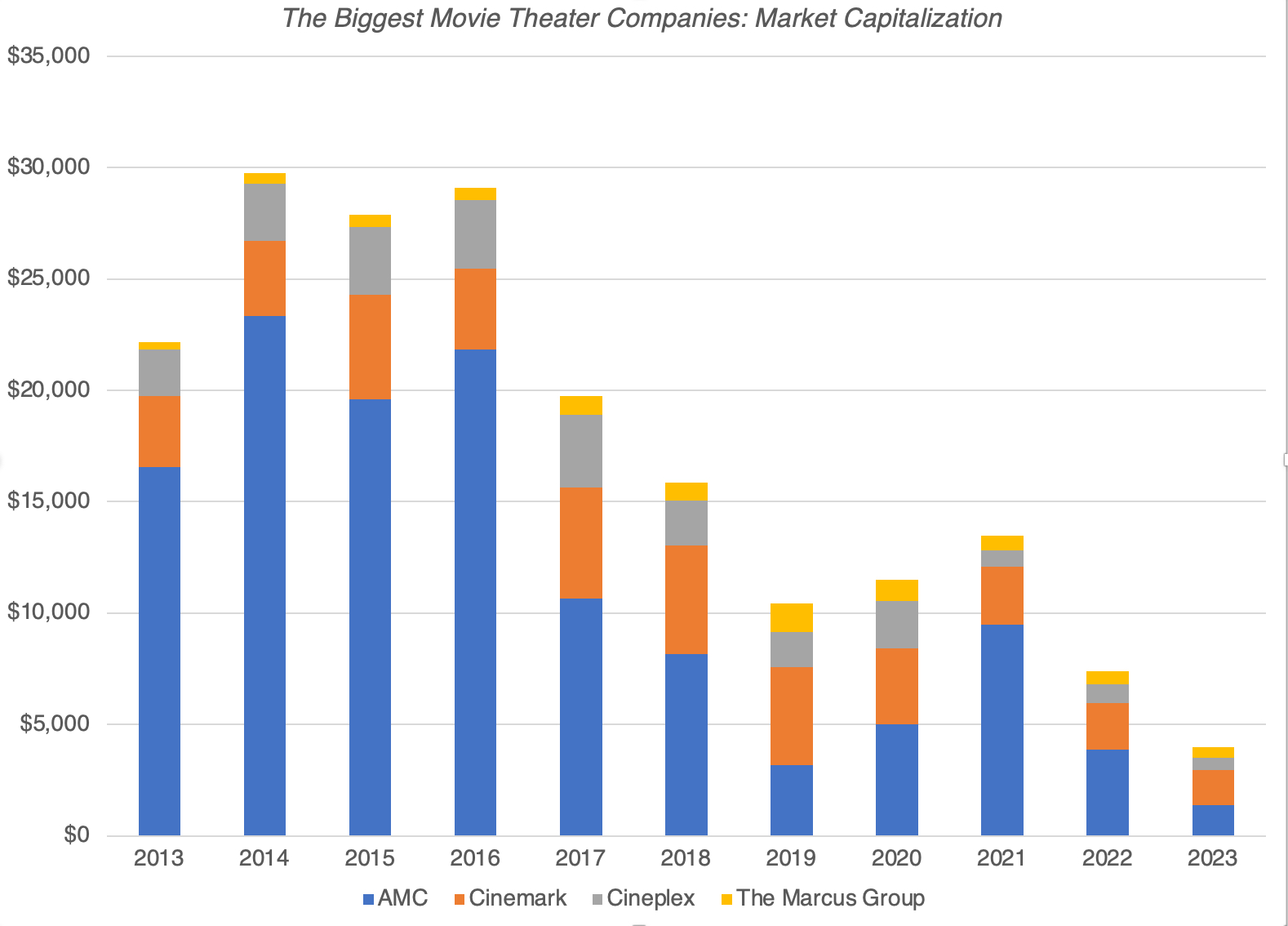

Whereas the shifts in worth from the established order gamers to Netflix and Dwell Nation is buffering the impression of streaming on the cumulative market capitalization of this business group, the market has change into decidedly extra unfavorable on one phase of this group – movie show corporations. Within the final graph, I take a look at the cumulative market cap of the 4 largest movie show corporations in North America – AMC, Cineplex, Cinemark and the Marcus Group.

Whereas the COVID shut down clearly impacted the 2020 numbers, be aware that the market decline in these corporations began in 2017, and has picked up steam since.

Company Governance

Company governance at corporations hardly ever attracts consideration through the good instances, the place managerial errors are neglected, and rising revenues and earnings can conceal company flaws. Nonetheless, in difficult instances, and disruption clearly has created challenges for leisure corporations, it isn’t shocking that we’re seeing extra investor angst at these corporations.

- CEO Turnover: There was drama within the prime ranks of Disney in the previous few years, as Bob Iger first turned over the reins within the firm to Bob Chapek in 2020, after which reclaimed it two years later. A few of that blowback might be traced to an costly wager made by the latter on streaming, reorganizing the corporate round Disney+, and investing billions into streaming content material, attempting to draw new prospects. Whereas there are elements particular to Disney that may make clear that firm’s CEO wars, I count on CEO turnover and turmoil to extend at leisure corporations, as traders look to interchange administration at corporations which are struggling, in a typically futile effort to alter their fortunes.

- Activist Presence: It’s no shock that activist traders are drawn to industries in turmoil, pushing corporations to spend much less on reinventing themselves and returning extra cash to shareholders. Right here once more, the Disney expertise is instructive, the place Nelson Peltz’s opposition to Chapek’s plans clearly performed a job within the CEO change this yr. Whereas Iger has been given some respiratory room to repair issues after his return, the clock is ticking earlier than activist traders return to the corporate. Actually, I count on the businesses within the leisure group to be prime targets for activist traders within the subsequent few years.

- Spin-offs, Divestitures and Break-ups: In response to streaming challenges, leisure corporations have began exploring whether or not splitting up or spinning of companies will enhance their probabilities of survival and success within the streaming age. Warner Bros. was spun off by AT&T and merged with Discovery in 2022, exactly for that reason, and the push for Disney to spin off or divest ESPN is equally motivated.

- Chapter: For the businesses whose financials have imploded on account of streaming, and all have debt, you need to count on to see dire information tales not nearly layoffs and shrinkage, however about potential chapter. Within the theater enterprise, this has change into actuality as Cineworld (proprietor of Regal, the second largest theater chain in North America) issued a chapter warning in early 2023, and AMC (proprietor or each the biggest theater chain and a streaming service) needed to do a reverse inventory cut up to maintain itself from careening in the direction of penny inventory standing.

There are three last notes that I want to add to this (lengthy) publish. First, I do know that this publish has been US-centric in its examination of the streaming results on leisure, however I do imagine that a lot of it applies to the remainder of the world, with a caveat. The established order could also be higher protected in different components of the world, both due to specific limits on or implicit obstacles to entry. Thus, streaming could also be much less of a direct menace to Bollywood, India’s immense homegrown movie-making enterprise, than it’s to Hollywood, however change is coming nonetheless. Second, as I famous earlier than, the road between content material made by professionals (film makers, broadcasting studios) and people (on platforms like YouTube and TikTok) is getting fuzzier, and they’re all competing for restricted viewer minutes. Third, for these on this enterprise who’re naive sufficient to assume that synthetic intelligence will rescue their corporations from oblivion, I’d supply the identical warning that I did to the energetic cash administration enterprise, just a few months in the past. If everybody has it, nobody does, and with AI, content material makers might very properly discover themselves competing with laptop energy and know-how corporations, and that’s not a battle the place they’ve the higher hand.

What the longer term holds…

The consequential and unresolved query is what the film and broadcasting enterprise will appear like a decade from now, because the reply will decide how stakeholders within the enterprise will likely be affected. To border the reply, I begin by trying on the most malignant and benign methods by which this might play out:

- At one excessive, you might even see the film and broadcasting enterprise comply with the music enterprise and see a collapse of revenues, a destruction of the established order and a resetting of the aggressive panorama. If this occurs, among the largest names in motion pictures and broadcasting will disappear as unbiased entities, both absorbed as items of a lot bigger corporations or stop to exist. The disruptors, together with Netflix and Dwell Nation, will face totally different challenges, as they now change into the established order, and so they must determine the right way to make their enterprise fashions worthwhile and sustainable, whilst they themselves will change into targets of recent disruptors.

- On the different exhibit, you will notice leisure proceed to develop as a enterprise, however with establishment gamers (content material makers and exhibitors) bringing their strengths into play to outflank the disruptors. On this situation, the massive names within the film and broadcasting enterprise will modify how they make and exhibit content material, and are available again, larger, stronger and extra worthwhile than they have been within the pre-streaming period.

- There’s a middle-ground, the place success would require that you simply draw on the strengths of each the established order and new applied sciences. The gamers in the established order who’re adaptable and prepared to alter will soak up these gamers who usually are not, and there will likely be an identical shake up amongst disruptors, with these disruptors who mix leisure enterprise knowledge with technological knowhow will win on the expense of disruptors who don’t.

As traders on this business group, your activity is straightforward, in the event you imagine in both excessive. When you imagine that disruption will likely be absolute and upend the film and broadcasting companies, you need to, on the minimal, keep away from the established order leisure corporations, and if you’re extra of a threat taker, promote quick on these corporations. When you imagine that in any case is alleged and achieved, disruption will develop leisure enterprise revenues, however will go away the established order on prime, you should purchase Disney, Warner and even perhaps AMC, and promote quick on the highest-flying newcomers within the enterprise.

If, like me, you go for the center floor, your success will rely on how good you’re at assessing adaptability in leisure corporations, shopping for establishment corporations with speedy studying curves on streaming and new applied sciences and disruptors that purchase content-making expertise to pair with technological prowess. That will make each Disney and Netflix works-in-progress, with the previous nonetheless wrestling with the problem of creating its streaming platform a money-maker and the latter engaged on a content material mannequin that’s extra disciplined and less expensive. I took a run at valuing each corporations, assuming that they every discover their option to a wholesome stability (between progress and income), with Disney’s margins settling in beneath the place the 18-20% ranges the corporate delivered in pre-COVID days, and Netflix decreasing its content material spending (with content material prices rising a lot slower than subscriber progress), going ahead:

| Disney | Netflix | |

|---|---|---|

| Revenues (LTM) | $87,807 | $32,465 |

| Working Revenue | $7,725 | $5,624 |

| Income Development (final yr) | 8.30% | 5.44% |

| Working Margin (LTM) | 8.80% | 17.32% |

| Anticipated Income Development (Yrs 1-5) | 10.00% | 15.00% |

| Anticipated Working Margin | 16.00% | 20.00% |

| Gross sales to Capital | 1.46 | 3.00 |

| Worth per share | $87.52 | $238.08 |

| Worth per share | $80.00 | $443.10 |

| Spreadsheet | Obtain | Obtain |

Put merely, the market appears to be pricing within the presumption that Netflix will proceed to get content material prices below management, whereas nonetheless delivering progress just like what it has delivered previously, whereas it’s pricing Disney for low progress and margins that can fall wanting their historic norms. I agree that Disney is a multitude, proper now, however I do imagine that at present pricing, the chances favor me extra with Disney than Netflix, however that’s simply me!

YouTube Video